The Housing Market

The Housing Market

Notes from a Pandemic boomtown

it’s just an itsy little gully, that’s all

Like, everybody said OK—that was crazy—let’s calm down

—The Big Short

I spent the pandemic between Sweden and North Carolina. Sweden was mostly normal—people kept living where they lived in their secured, rent-stabilized apartments, few people wore masks, bars closed at 8, then 11, then 2, and the kids kept going to school, physically going to school. Anders Tegnell said keep calm and carry on and that's mostly what people did. But in my mother and brother’s brick-ranch-house quiet suburb in NC, something strange started happening in late 2020. I take my brother trick-or-treating most years, it’s an important tradition for our family. The elderly neighbors depend on it, like the Pony Express, they stay up, they have their candy ready and say, “It wouldn’t be Halloween if you didn’t come by!” Between 2015 to 2019, the Halloween ambiance and decorations in our leafy suburban neighborhood reached its lowest ebb in my lifetime. Most of the residents were empty nesters with adult children living in the cities, with a few divorced and single people in their 40s distributed here and there. There were almost no 30-somethings, very few young kids.

Then the deluge. All of a sudden, seemingly out of nowhere, the neighborhood was repopulated with young transplant families. Walking with their kids and inlaws in big packs (the big happy white families infuriated me, while I found it heartwarming and American if they were Indian or Somali or Asian), moms and dads my age on runs with their golden retrievers, black Range Rovers, indie couples sweating in the front yards obsessing over their landscaping. After the first lockdown autumn, the next Halloween, it was lively, a real proper Halloween with huge packs of kids trick-or-treating.

The license plates didn’t indicate they relocated from any one specific state (or maybe they were savvy enough to realize that interstate hostility had emerged, specifically towards New York and California and changed quickly to NC plates) but yeah, more Teslas, more Instacart, more REI curbside pick-ups in futuristic overhead-door-opening space-cars, more signs of tech worker money and the New Millennial Suburbandom.

Where had they all come from? I don’t know. Did they have to all come here, to our temperate pine-needle Shire?

In retrospect, they seem like geniuses.

At peak pandemic while the rest of us were fretting about killing our loved ones and wearing rubber gloves and bleaching our nasal cavities, these people were moving into the old suburban neighborhoods and buying already-relatively-cheap houses at gorgeous 2.5% mortgage rates.

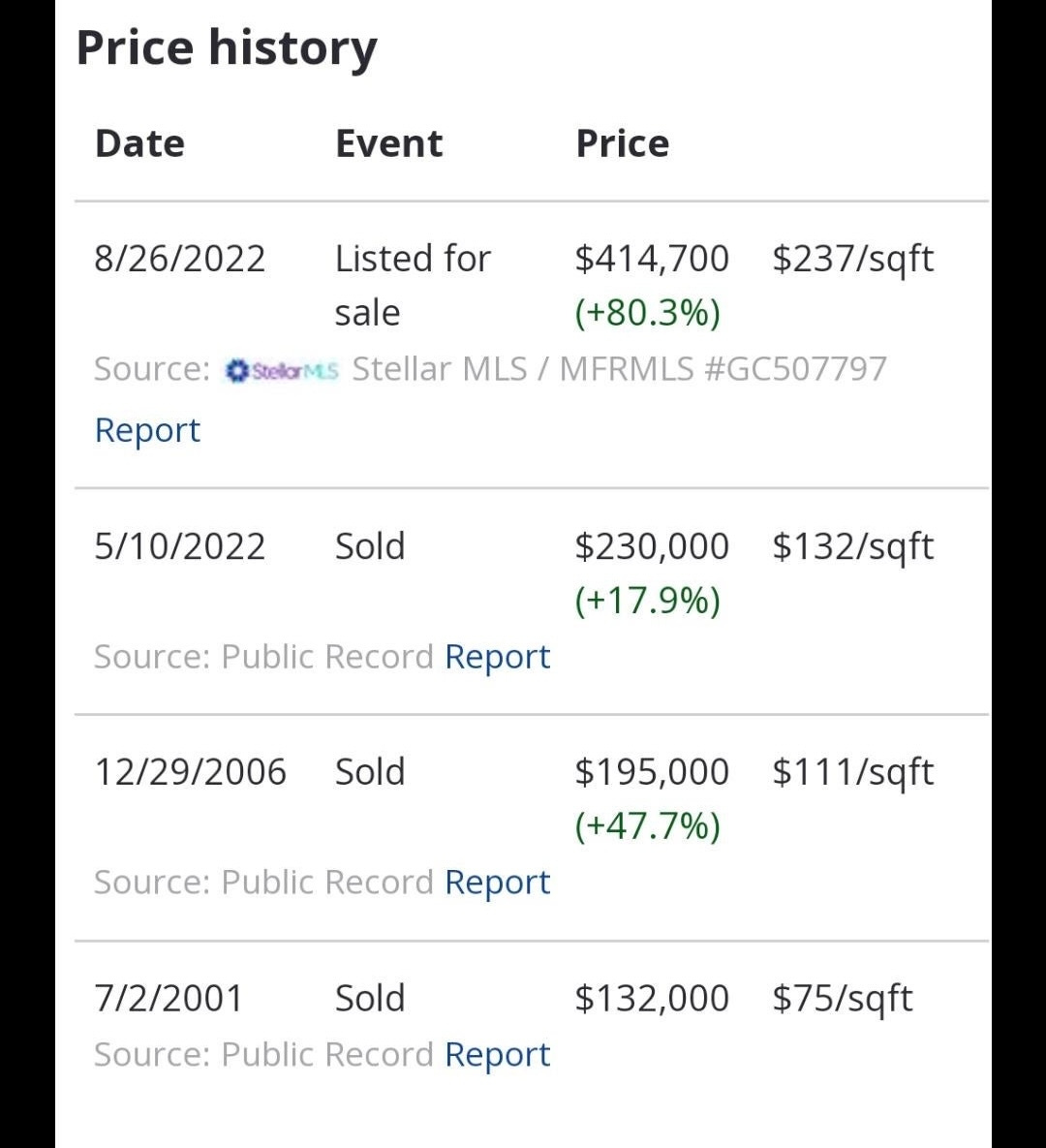

Every one of these houses has at least doubled in “Zestimate” value in the last two years, going from average about 200K to 400K. So these people got to work-remote in good climate, a pretty mild lockdown regime, low monthly payment, and can cash out with 200K in their pocket whenever they decide they need to go back to wherever. If they have kids, I’m sure the closed schools was stressful and destabilizing, but overall, how can you say the pandemic was bad for these people? Move to a beautiful safe place where they don’t have to show their vaccination card constantly and basically get paid double to do it.

Some will stay for good, obviously, they love going to the garden section at Lowe’s. A realtor told me that a lot of them had done what’s called a “live-in flip.” Ie. In 2020, they got a primary residence loan with 5% down payment and made some minor improvements while living in and enjoying the house. Smart, fiendishly smart. I guess most that didn’t cash out already will probably stay in their houses because their grandfathered-in mortgage payments are a lot lower than rents and 6% mortgage rate payments now, but if they had wanted to cash out in April 2022, they could have, easily, at peak prices.

Raleigh area and Asheville have become insanely hot places to live, drawing a huge influx, who come for a variety of good reasons—Raleigh has actual upward-middle-class jobs in sectors like nursing available in addition to the tech and gaming companies building campuses everywhere (most will be completed around 2023 and 2024). Asheville is the more boutique “work-from-home” option, probably more for people with unique diets and lifestyles who have truly remote knowledge jobs, because aside from tourism and service and real estate there is no middle-class economy there to speak of (Since the 1920s, Asheville always has been—and in my mind, always will be—a strange class-collision between the very rich progressive outsiders and very poor conservative natives).

Then there are the flippers—I’m talking about the Youtube-video 30-something MLM flipper couples. Some, I’m sure, did very well, but I talked to one guy who was selling a beautiful shell of a house in my neighborhood for around $265K. He had permitted the $200K gut renovation. It seemed absolutely insane because, when all was said and done, whoever bought it would put in $465K to own a small-ish house that would never sell above that. But it sold to some poor soul who I hope plans to live there a long time, they’re putting the finishing touches on it, it looks really nice.

And then of course the realtors. Many people went and got their real estate license during the pandemic. I definitely looked into it. The well-established broker-agents took out PPP loans and some, in high cost of living areas, had the best financial year of their lives in 2021 on the back of high sales and insane bidding-war inflated home prices.

Those of us that did not buy low-mortgage-rate homes feel like morons. Rents have gone up like crazy. Shittier and shittier homes are listed at worse and worse prices.

Where is this all going?

They’re calling it a “seller’s strike.”

The bidding wars and high cash direct payments to sellers have somewhat stopped, the houses are sitting on the market at high prices, but realtors and sellers are using all sorts of psychological tricks to try to keep the straight-line-up trajectory in their areas—these past few weeks it looks like the strategy is to continue to slash overpriced prices to give naive or desperate buyers the “you’re getting a good deal” feeling. But the good houses are still (mysteriously) going in a few days, over asking price.

The mortgage brokers all of a sudden seem very very eager to connect, because their whole industry is in freefall because…no one wants to or can take out a mortgage and pay double per month what they would have had to last year.

The experts are split are where things go from here, but it looks like stagnation—if you have a good house with a low mortgage rate, why sell and move if you don’t absolutely have to, when you’ll likely be moving down on the totem pole?

The late-adopting (post-2021 Bonanza) flippers (who use the so-called BRRRR Method) seem like they’re not going to make it. Many flippers rely on extremely-high-interest-rate “hard money” private loans which are not meant to actually really be paid beyond the 3-6 month period they renovate the house and they’re relying on a high appraisal and quick sale or rent once they make their improvements. If there’s no quick sale or high appraisal, they’re fucked. Even if they took out a regular mortgage at 6%, those payments have doubled, which means they’ll have to attempt to pass high rents (ie. their shitty mortgage) on to tenants, who just may not countenance $2400 a month to live in an Pandemic Boomtown that they really liked during remote-work-only at $1200 a month.

I’m also skeptical that the highly leveraged multiple-AirBnB moguls will survive, unless they are in a serious metro tourism area or vacationers area and locked in all their properties at 2.5% rates.

Eight or ten years ago, AirBnB was a place you could find unique places to crash cheaper than a hotel. I rented out my place in Brooklyn on AirBnb to interesting people. If you’ve checked it out recently, you can see it is now clearly dominated by investors gray, soulless “income generating AirBnBs” where they charge $100 a night for a one bedroom townhouse or guest suite plus $170 cleaning plus $55 in service fees, I mean fuck that, just get a $80 hotel with breakfast on Booking.com. AirBnB-as-income-generation will get more and more cracked down on in metropolitan areas, it might work long-term for big vacation houses that extended families want to rent for a week, but those looking for a night or two to crash will just go elsewhere unless it’s one of those “incredibly unique underwater Aurora Borealis igloo” AirBnB “experiences.”

The past couple of months, I have been lurking on a subreddit called r/ReBubble. It has grown exponentially and is a very heady collection of extremely angry individuals—it seems like half of the participants are embittered, hard-left millennial renters who loathe landlords and AirBnB. And half are Austrian Economics “abolish the Fed” free market purists—these two polar opposites have made a strange bedfellows pact together on hating on AirBnB and screenshotting flippers ridiculous home prices and hating on anyone who bought a house in 2020 and trying to sell it for double, and they are all amped up waiting for their chance to own a home after a big 2008-style Crash that they are predicting will always be happening soon, soon.

When 99% of people are primed and amped up for something good to happen for them, for the big “chance” they’ve been waiting for that they’re modeling on statistics, you can almost guarantee it won’t happen.

I think it is interesting and often funny but also its kind of sad, this certainty they have that this crisis will be just like the last crisis but this time they’ll be ready, and you’ll get this once-in-a-lifetime opportunity to buy a home on the cheap if you time it perfectly. Last time you were too young. Or didn’t have the money. Or you didn’t pull the trigger. Many of them are trying to redo the Big Short by short-selling Zillow and Opendoor stocks. This “crisis” (if it becomes a real crisis) probably won’t be like the last crisis—even if home prices go down, best case scenario they get back to where they were before the pandemic. We’re probably not going back to the forced selling, bargain-basement-prices of 2010-2012.

There is no trick, no well-worn path (everyone suddenly thinks they’re the second coming of Michael Burry) that everyone is going to be able to get everyone where they want to go, which is to a place of security.

I think the new Millennial desire to be owners-not-renters is by no means exhausted, they are going to keep going no matter what, as they have families they will continue to bid up prices on instagrammable mid-century-modern fixer uppers in 2nd city pandemic boomtowns whenever they appear, they don’t care about comps, they don’t care about the home’s actual value. They don’t want to live in the city center anymore, but they also don’t want to live in the country-country, they want purple areas, they want Durham, one-third country, one-third queer Ivy League, one-third black, or they’re going to return home, like turtles, to spawn in their native habitat of the suburbs. If people wanted financial independence and security in a place to live, in May of 2020, they would have been signing their 2.5% mortgage documents on a spacious but affordable house in Austin or Boise or wherever, and if they didn’t do that (I didn’t do that, some people did) they probably didn’t do it because they had been waiting a decade for a once-in-a-lifetime pandemic to hit and their job to let them go remote and the Fed to loosen financial conditions so they could move their family to Austin, they probably just did it because it seemed like the next reasonable thing to do.

Housing is not for rocket scientists, for those trying to model out the exact right moment to buy or the perfect leverage to get a good deal on rent, people just need and want and will continue to make moves on places to live.